When you're managing a chronic condition like rheumatoid arthritis or Crohn’s disease, the cost of your medication shouldn’t be the biggest hurdle to getting better. But for many patients in the U.S., switching from a brand-name biologic to a biosimilar - a highly similar, lower-cost version - is anything but simple. Even though biosimilars have been approved by the FDA since 2015 and are proven to be just as safe and effective, insurance coverage practices often make them harder to access than the original drug.

What Are Biosimilars, Really?

Biosimilars aren’t generics. Generics are chemically identical copies of small-molecule drugs like metformin or lisinopril. Biosimilars, on the other hand, are made from living cells - like proteins, antibodies, or enzymes - and are incredibly complex. Think of them as near-identical twins of biologic drugs, not exact copies. They’re designed to match the reference product in safety, purity, and potency, with minor differences allowed because biological systems aren’t as predictable as chemical synthesis.

The first FDA-approved biosimilar was Zarxio in 2015, a version of Neupogen used to boost white blood cell counts. Since then, over 70 biosimilars have been approved, with about 40 currently on the market. The most common ones target conditions like arthritis, diabetes, and cancer. Adalimumab biosimilars - alternatives to Humira - are among the most widely approved, with eight different versions now available.

But approval doesn’t mean access. And that’s where insurance comes in.

How Insurance Plans Handle Biosimilars

Most private and Medicare Part D plans use a tiered formulary system to control costs. Drugs are grouped into tiers based on price and clinical use. Tier 1 is usually generic pills with low copays. Tier 4 or 5 is where biologics live - the expensive ones that require special handling and monitoring.

Here’s the problem: 99% of Medicare Part D plans in 2025 placed Humira and its biosimilars on the same tier. That means if you switch from Humira to a biosimilar, your out-of-pocket cost barely changes. A patient paying $1,200 a month for Humira might pay $1,150 for a biosimilar. That $50 difference doesn’t motivate anyone to switch.

Worse, less than 1.5% of plans put biosimilars on a lower tier to encourage use. In contrast, brand-name biologics like Humira are still covered by nearly all plans - even though multiple biosimilars exist. Only 50% of Medicare Part D plans cover any biosimilar at all, according to JAMA Network data from June 2024.

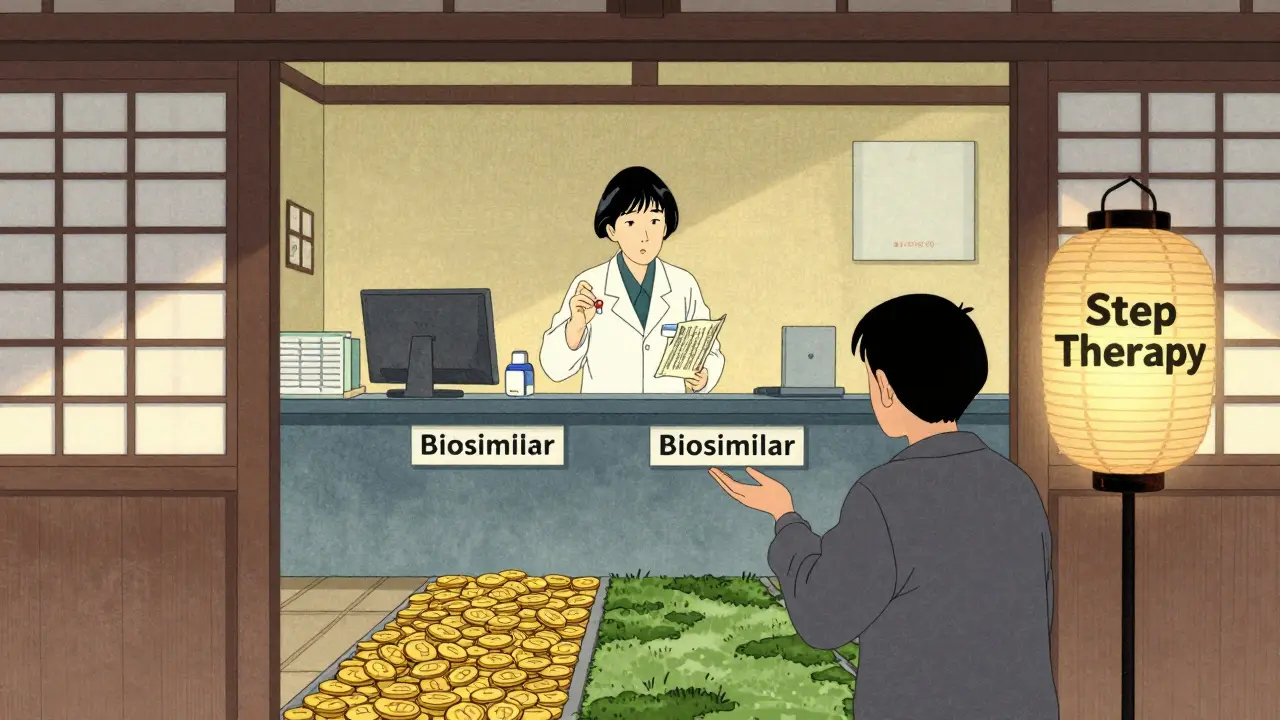

Prior Authorization: The Hidden Gatekeeper

If you’re lucky enough to have a biosimilar covered, you still have to jump through hoops. Prior authorization (PA) is required for 98.5% of plans that cover both Humira and its biosimilars. That means your doctor has to submit paperwork - often including lab results, treatment history, and proof that other drugs failed - before the insurer approves the prescription.

And here’s the twist: PA requirements are just as strict for biosimilars as they are for the original drug. There’s no faster or easier path for the cheaper option. In fact, some insurers require patients to try a biosimilar first before even considering the brand-name drug - a practice called step therapy. One rheumatology case study showed a patient waiting 28 days for treatment because they had to fail a biosimilar trial before getting approved for Humira.

Doctors are drowning in this paperwork. A 2024 survey found that 78% of rheumatologists spend 3 to 5 hours per week just managing prior auth requests. That’s time not spent with patients.

Why Don’t Insurers Push Biosimilars Harder?

At first glance, it seems like a no-brainer. Biosimilars cost 10-33% less than their reference products. The Congressional Budget Office estimates they could save the U.S. healthcare system $54 billion over the next decade. So why aren’t insurers lining up to promote them?

The answer lies in how pharmacy benefit managers (PBMs) - the middlemen between insurers and pharmacies - structure their deals. PBMs often negotiate rebates from brand-name drug makers. These rebates can be huge, and they’re sometimes tied to exclusivity. If a PBM puts a biosimilar on the preferred tier, it risks losing those rebates.

Some PBMs have started changing tactics. Express Scripts, OptumRx, and CVS Caremark now exclude Humira entirely from their 2025 commercial formularies. Instead, they push patients toward biosimilars by placing them on preferred specialty tiers (Tier 3) with lower coinsurance - 25% instead of 33%. It’s not about fairness; it’s about leverage. By removing the original drug, they force the switch.

But this strategy isn’t universal. UnitedHealthcare, Cigna, and Centene still don’t cover any insulin biosimilars, even though biosimilars for insulin are approved and available. And when biosimilars are covered, they’re often stuck on the same high-cost tier as the brand-name drug.

The Real Cost to Patients

For patients, the financial impact is real. Even with insurance, many pay hundreds - sometimes over $1,000 - per month for biologics. With coinsurance rates of 25-33% on specialty tiers, a $5,000 monthly drug means $1,250-$1,650 out of pocket. That’s more than many people earn in a week.

And because biosimilars are rarely on lower tiers, the savings are minimal. A Medicare Rights Center analysis found that patients switching from Humira to a biosimilar save only about $50 a month on average. That’s not enough to overcome fear, confusion, or the hassle of switching.

Patients also face delays. If your doctor prescribes a biosimilar but your insurer requires prior auth, you might wait two weeks for approval. In the meantime, your condition worsens. For someone with severe arthritis or inflammatory bowel disease, that delay can mean more pain, more flare-ups, and more emergency visits.

What’s Changing in 2025?

There are signs of progress. In late 2024, the Office of Inspector General (OIG) found that most Medicare Part D plans still didn’t incentivize biosimilar use. That report pushed CMS to expand its formulary monitoring to include tier placement comparisons between biosimilars and reference products.

Some PBMs are now using exclusionary formularies - removing the brand-name drug entirely - to force adoption. This approach has worked in Europe, where biosimilars make up over 80% of the market for drugs like Humira. In the U.S., biosimilar market share for adalimumab is still just 23%, despite eight available options.

Industry analysts predict that by 2027, biosimilar adoption could hit 40% if PBMs continue shifting toward exclusionary models and CMS enforces fair tiering rules under the Inflation Reduction Act. But without policy changes, we’ll keep seeing the same pattern: biosimilars approved, but not promoted.

What Can You Do?

If you’re on a biologic and your doctor suggests a biosimilar:

- Ask your insurer if the biosimilar is on a lower tier - if not, request a formulary exception.

- Check if your plan excludes the brand-name drug. If it does, you may have no choice but to use the biosimilar.

- Ask your pharmacist if the biosimilar is interchangeable (meaning they can substitute it without asking your doctor). Only a few biosimilars have this designation.

- Document any delays or denials. If your treatment is held up, contact your patient advocate or state insurance commissioner.

Providers can also push back. Submit appeals, document administrative burden, and advocate for tier placement changes during your health plan’s annual review period (October to December). Change doesn’t happen overnight - but it starts with asking the right questions.

Why aren’t biosimilars cheaper if they’re supposed to save money?

Biosimilars are cheaper to produce, but insurers often don’t pass those savings to patients. Many plans place biosimilars on the same high-cost tier as the original drug, so out-of-pocket costs stay nearly identical. PBMs also negotiate rebates from brand-name manufacturers, which creates financial incentives to keep the original drug on formularies.

Can a pharmacist switch my Humira to a biosimilar without asking my doctor?

Only if the biosimilar has an "interchangeable" designation from the FDA. As of 2025, only a few adalimumab biosimilars - like Cyltezo - have this status, and even then, it only applies to low-concentration formulations. Most biosimilars still require a new prescription from your doctor.

Do all insurance plans cover biosimilars?

No. In 2025, only about half of Medicare Part D plans covered any biosimilar for Humira, and even fewer covered insulin biosimilars. Private insurers vary widely - some exclude biosimilars entirely, while others restrict them to prior authorization or step therapy.

Why do I have to try a biosimilar before getting the brand-name drug?

This is called step therapy. Insurers use it to control costs by requiring patients to try the cheaper option first. But it can delay treatment, especially for patients with severe conditions. Many providers argue it’s clinically inappropriate when the original drug is the most effective option.

Is there a way to fight an insurance denial for a biosimilar?

Yes. You can file a formal appeal with your insurer, often with support from your doctor. Include clinical documentation showing why the biosimilar won’t work for you - or why the brand-name drug is medically necessary. Many appeals succeed, especially when backed by medical evidence. You can also contact your state’s insurance commissioner for help.

8 Comments

Man, I’ve seen this play out in India too - even when biosimilars are available, the system doesn’t make it easy. Doctors here get pressured by pharma reps to stick with the brand, and patients? They’re stuck between fear and cost. I had a cousin on Humira for RA, switched to a biosimilar, and her copay didn’t drop a dime. The insurance didn’t care about savings - they just moved the same price tag to a different label.

It’s not about the science. It’s about who’s getting paid behind the scenes. PBMs aren’t villains - they’re just following the money. But that money isn’t coming from patients. It’s coming from our future health.

And yet, here we are. Still waiting for the system to wake up.

so like… are u telling me the FDA approved these biosimilars but the insurance co’s are still pushin’ the expensive one? lol. i swear this is how the system works. they dont want you to get better, they want you to be a customer for life. biologics = lifetime subscription. biosimilars = one-time purchase. who wins? the guy who sells the original. not you. not me. not the patient.

its not a health care system. its a profit system. and we’re all just data points with a pulse.

It is my professional opinion, based on a comprehensive review of regulatory, economic, and administrative data, that the current structural disincentives embedded within the pharmacy benefit management (PBM) reimbursement architecture represent a systemic failure of fiduciary responsibility to the insured population. The continued placement of biosimilars on identical cost tiers as reference biologics, coupled with the pervasive use of prior authorization protocols that are functionally indistinguishable between interchangeable and non-interchangeable products, constitutes a de facto market distortion that violates the principles of evidence-based formulary design.

Furthermore, the reliance on manufacturer rebates as a primary driver of formulary placement is not merely inefficient - it is ethically indefensible. This model incentivizes the perpetuation of higher-cost therapeutics, directly contravening the statutory intent of the Inflation Reduction Act and the public health mission of Medicare Part D.

Without mandatory tier segregation and transparent rebate disclosure, we are not reforming healthcare - we are merely rebranding exploitation.

Here’s the simple version: biosimilars cost less to make, but insurers don’t pass that savings to you. Why? Because the middlemen - PBMs - get paid big bucks by the big drug companies to keep the expensive version on the list. So even if a biosimilar is half the price, your copay stays the same.

Some plans are starting to fix this by removing the brand-name drug entirely. If Humira’s gone, you have no choice but to take the biosimilar. And then - finally - you save money.

Bottom line: it’s not about safety. It’s about money. And the system is rigged. But change is happening. Slowly.

Ugh. Another post about how ‘the system is broken.’ Newsflash: it’s not broken. It’s working exactly as designed. Insurance companies aren’t evil - they’re just doing what any rational business would: maximizing profit. Patients think they’re being ‘exploited’? Maybe they should’ve read the fine print before signing up.

Also, why are we even talking about biosimilars? If you can afford a biologic, you’re already in the 1%. The real problem is that we let people think medicine should be cheap. It’s not. It’s expensive. Get over it.

And stop pretending this is about ‘access.’ It’s about entitlement.

I just want to say - as someone who’s been on a biologic for over a decade - that the emotional toll of this system is just as heavy as the financial one. You’re not just fighting insurance paperwork. You’re fighting fear. Fear that if you switch, your body will reject it. Fear that your doctor won’t advocate for you. Fear that if you ask for help, you’ll be labeled a complainer.

I’ve cried in waiting rooms. I’ve sat in my car for an hour after a denial letter because I didn’t know what to do next. I’ve called my mom at 2 a.m. just to say, ‘I don’t know if I can keep doing this.’

And yes, I know biosimilars are safe. I’ve read the studies. But safety doesn’t fix the loneliness of being told your body is too complicated to be trusted with a cheaper option. The system doesn’t see you as a person. It sees you as a risk profile.

So if you’re reading this and you’re going through this - I see you. And I’m sorry it’s this hard. You deserve better.

So let me get this straight - the government approved biosimilars, doctors say they’re just as good, and patients want them… but insurers still make you jump through a flaming hoop just to get the cheaper version?

Wow. I didn’t know healthcare was a game of ‘pass the buck’ with a side of corporate greed.

And yet, here we are in 2025, still pretending this is about ‘clinical outcomes’ instead of ‘who got the biggest rebate check.’

At this point, I’m just waiting for the PBM to start charging us extra for breathing. ‘Sorry, you’re on a biosimilar? That’s a Tier 4 perk. You’ll need to pay $200/month for oxygen.’

The system is rigged. PBMs control everything. Formularies are not medical decisions. They’re financial ones. No one is talking about the real issue: rebates. Remove them. Force tier separation. End prior auth for biosimilars. Do it now. No more delays. No more excuses.